Budget 2026 Explained: How the Minimum Wage Rise to €14.15 and USC Band Changes Affect Your Pay

Budget 2026 Explained: How the Minimum Wage Rise to €14.15 and USC Band Changes Affect Your Pay

Feb 09, 2026

At the same time, updated USC bands and related tax measures in Budget 2026 will decide how much of that higher wage you actually keep in your pocket.

Key Takeaways

| Question | Answer |

|---|---|

| What is the new minimum wage from 1 January 2026? | The statutory national minimum wage rises to €14.15 per hour, affecting full‑time and part‑time workers and driving adjustments to USC bands. |

| How is USC changing in Budget 2026? | The 2% USC band ceiling increases by €1,318 to €28,700 so full‑time minimum wage workers remain within the lower USC rate. For tailored advice, our tax planning service in Limerick explains how this impacts your net income. |

| Will I pay USC if I am on very low income? | No USC applies where your annual income is €13,000 or less, so some very low‑paid or part‑time workers still fall outside USC altogether. |

| What are the main USC rates for 2026? | The published structure is: 0.5% up to €12,012, 2% from €12,012.01 to €28,700, 3% from €28,700.01 to €70,044, and 8% above that level. |

| How can employers manage higher wage and USC costs? | We usually recommend reviewing payroll, margins, and forecasting together. Our dedicated payroll services in Limerick help employers update systems and stay compliant. |

| Does Budget 2026 change anything else for workers? | Yes, measures like the extended Rent Tax Credit and Mortgage Interest Tax Relief support take‑home income alongside the higher minimum wage and rebalanced USC. |

| Where can small businesses get help understanding Budget 2026? | We work with startups, SMEs and contractors to assess wage, USC and VAT impacts through our budgeting support service and wider advisory. |

Overview of Budget 2026: Why the Minimum Wage and USC Are Changing Together

For many clients we work with, the key question is not just the headline wage figure but how USC, income tax and credits interact in practice. We focus on how these measures play out in net pay, payroll costs, and longer‑term financial planning for both employees and businesses.

Policy goals behind the package

At the same time, extensions of the Rent Tax Credit, Mortgage Interest Tax Relief and reduced VAT on energy form a support framework that complements the wage and USC changes. We see this as part of a broader cost‑of‑living strategy rather than a stand‑alone wage decision.

Who is most affected by the changes

The direct effects are greatest for those on or near the minimum wage and for employers with large numbers of lower‑paid staff. Sectors like hospitality, retail, cleaning, and some contracted services will feel the strongest payroll impact.There are also significant implications for self‑employed workers who benchmark their rates against minimum or low‑wage employment norms. Contractors, sole traders and freelancers must consider their pricing and tax planning in light of the updated USC structure.

New Minimum Wage of €14.15: What It Means for Workers and Employers

From 1 January 2026, the national minimum wage increases to €14.15 per hour, which for a standard 39‑hour week equates to just under €28,800 a year before tax.For workers, this is a clear upward shift in gross pay, but net income still depends on USC, income tax and PRSI.

For employers, the higher hourly rate becomes the baseline for all payroll budgeting, contract reviews and pricing decisions from 2026 onwards.

We advise businesses to run detailed pay simulations early, so they can adjust overtime rates, differentials and salary bands in an orderly way.

Impact on full‑time and part‑time staff

A full‑time worker on the old minimum wage will see a clear rise in gross earnings, which can significantly improve affordability once USC and income tax are accounted for.Part‑time workers may move from below to above the USC exemption threshold of €13,000, which can trigger a first USC liability.

We encourage employees to review their projected 2026 pay slips so they can anticipate actual net income and adjust budgets for rent, mortgage and other costs.

Employer payroll strategies for 2026

Many employers will need to revisit pay scales that sit just above minimum wage to maintain fair differentials and staff motivation. The new minimum rate also feeds into overtime,Sunday premium and certain contractual allowances that are calculated as multiples of the basic rate.

Using our payroll support, we help clients model multiple scenarios, from zero‑hours contracts up to structured salary bands. This reduces the risk of sudden cost shocks midway through the year.

The USC structure for 2026 has been adapted to prevent full‑time minimum wage workers from drifting into higher USC bands simply because their hourly rate rose.

USC Band Changes in 2026: Keeping Pace with €14.15 per Hour

The key move is to lift the upper ceiling of the 2% band by €1,318, to a new limit of €28,700.

This aligns the 2% band with the annual earnings of a full‑time worker on €14.15, working a typical full‑time schedule. In practice, this protects minimum wage workers from being taxed at a higher USC rate on part of their income.

The detailed USC band structure for 2026

USC will apply on gross income above €13,000 per year, with the following main bands and rates:- 0.5% on income up to €12,012

- 2% on income from €12,012.01 to €28,700

- 3% on income from €28,700.01 to €70,044

- 8% on income above €70,044

Why the 2% band increase matters

Before Budget 2026, successive minimum wage increases risked pushing low‑wage workers into higher USC rates, eroding net gains. By raising the 2% band ceiling to €28,700, government has tried to prevent that creep for a standard full‑time minimum wage worker.In our experience, this is one of the most important but often overlooked details for both payroll planning and employee expectations. Workers see the €14.15 headline, but actual pay packets reflect the combined effect of income tax, USC, PRSI and credits.

To make the numbers concrete, we usually walk clients through simplified examples that show the combined effect of minimum wage, USC and other deductions.

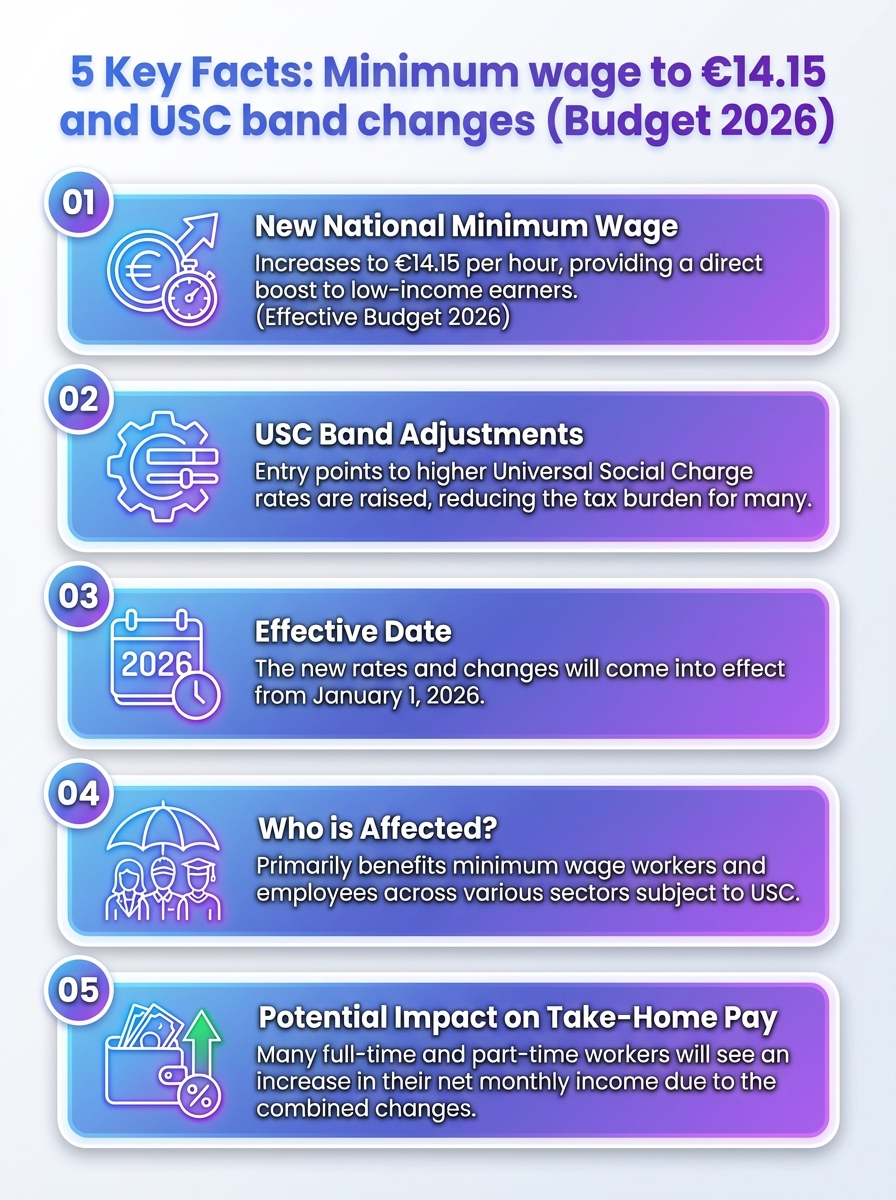

Quick visual overview of Budget 2026: the €14.15 minimum wage rise and USC band changes. Five key facts explained for easy understanding.

Did You Know?

USC rates and bands for 2026 will be: 0.5% up to €12,012; 2% on €12,012.01–€28,700; 3% on €28,700.01–€70,044; 8% above; and no USC at all for incomes of €13,000 or less.

Take‑Home Pay Examples: How Much of €14.15 You Actually Keep

The exact results depend on individual circumstances, including credits and PRSI, so the figures below illustrate direction rather than exact outcomes.

Consider a full‑time worker on €14.15 for 39 hours a week. Their annual gross pay is just under €28,800, which keeps them entirely within the adjusted 2% USC band and avoids the 3% rate that applies above €28,700.

Illustrative USC calculation at €14.15 per hour

At that income level, USC is charged at 0.5% on the first €12,012 and 2% on the balance up to the €28,700 ceiling. Since the worker’s income is slightly above €28,700, only a narrow slice would actually be in the 3% band, and careful band design aims to limit this effect.If hours or overtime lift annual pay significantly beyond €28,700, a greater share of income moves into the 3% band. For this reason, we encourage both workers and employers to understand where typical annual hours place each employee within the USC structure.

Comparing old and new positions

Without the 2% band increase, more of a full‑time minimum wage earner’s income would have fallen into the 3% band, raising their overall USC burden. Budget 2026 ensures that most of the statutory wage increase is retained by workers through a moderation of USC.We support clients with custom take‑home pay reports that factor in credits, other income sources and reliefs. This is often particularly helpful for employees considering additional hours or second jobs in 2026.

The minimum wage and USC adjustments do not exist in isolation. Budget 2026 extends and refines several other supports that directly affect net disposable income, especially for low and middle earners.

Budget 2026 Supports Beyond Wages and USC: Rent, Mortgage and Energy

Key among these is the extension of the Rent Tax Credit to 2026, 2027 and 2028, worth up to €1,000 for single renters and €2,000 for jointly assessed couples each year. For many workers on or near minimum wage, this credit can offset rent increases and improve overall affordability.

Mortgage and housing‑related measures

Mortgage Interest Tax Relief is extended to 31 December 2026, with a credit of up to €1,250 for 2025 and €625 for 2026 per qualifying property. For working households, this offsets part of the pressure of higher interest costs at a time when wages and USC are also evolving.On the supply side, a reduced 9% VAT rate on the sale of completed apartments, along with enhanced 125% corporation tax deductions for certain apartment‑related costs, aims to improve housing availability. Over time, greater supply can ease rent and price pressures for workers whose wages are governed by the new €14.15 minimum.

Energy VAT and ongoing cost‑of‑living support

The 9% VAT rate on gas and electricity is extended to 2030, which reduces some of the volatility in energy bills for households and businesses. This interacts with wage and USC changes by helping stabilise one of the major recurring expenses in family budgets.We encourage clients to consider all these measures together, rather than focusing only on the wage increase. In many cases, the combination of USC relief, rent or mortgage credits and energy VAT support makes a noticeable difference to overall financial resilience.

From an employer’s perspective, the Budget 2026 changes require timely payroll updates and clear employee communications. We help clients update payroll software settings, revise pay templates and ensure that the new USC bands are correctly reflected in deductions from the first 2026 payroll run.

Did You Know?

The USC 2% rate band ceiling will rise by €1,318 to €28,700 in 2026 so that full-time minimum wage workers on €14.15 per hour largely remain within the lower USC bracket.

Payroll Compliance: Updating Systems for €14.15 and New USC Bands

HR teams also need to review contracts, staff handbooks and any documented pay structures that reference the minimum wage. Aligning documentation with the new statutory rate reduces the risk of disputes and ensures clarity for staff.

Early testing avoids under‑ or over‑deduction of USC in January and February payrolls, which can create unnecessary queries and corrections.

Key payroll tasks before January 2026

We recommend that businesses complete the following steps well before the end of 2025:- Update hourly and salary rates to at least €14.15 where required.

- Implement the 2026 USC bands in payroll software and test calculations.

- Review overtime, allowances and premium rates linked to the basic wage.

- Check that staff on training or youth rates still comply with legislation.

Communicating changes to staff

Clear communication helps staff understand that a higher gross wage does not equal a euro‑for‑euro increase in net pay. We help employers prepare concise explanations and sample payslips that show workers how the new USC bands protect most of the gain from the wage rise.This transparency builds trust and reduces confusion or disappointment when staff compare expected and actual take‑home pay in early 2026.

Contractors and Sole Traders: Pricing and USC in a Higher‑Wage Economy

Contractors, tradespeople and sole traders are not paid the minimum wage in the same way as employees, but the statutory rate still influences market expectations and pricing. When employees in your sector move to €14.15 and beyond, clients and workers often benchmark contractor rates against that floor.We work with contractors to understand how USC and income tax apply to their profits, not just turnover, under the 2026 structure. This helps them quote rates that reflect both market realities and their true after‑tax income needs.

USC planning for self‑employed incomes

Self‑employed individuals pay USC on their total income above €13,000 using the same 2026 band structure as employees. Higher hourly or day rates may be required to maintain net income once tax, USC and expenses are factored in.We help sole traders optimise expense claims, pension contributions and payment timings so that their effective tax and USC burden is sustainable relative to their market rates.

Adjusting pricing in line with Budget 2026

As labour costs rise throughout the economy, contractors may face increased input costs for subcontracted labour or services. We advise reviewing contracts and pricing annually, with Budget 2026 serving as a natural trigger point for an updated pricing strategy.In our experience, transparent cost‑based explanations for price adjustments are more acceptable to clients than unexplained hikes. Linking these explanations to statutory wage and USC changes helps frame conversations constructively.

The direct effects of the €14.15 minimum wage and USC changes vary significantly by sector. Hospitality and retail, where a high share of staff are paid close to minimum wage, face a larger proportional increase in payroll costs.

Sector‑Specific Effects: Hospitality, Retail and High‑Wage Sectors

In contrast, sectors where wages are already well above minimum, such as certain professional or technology roles, will feel the USC band changes more as a marginal adjustment rather than a core cost shift.

Labour‑intensive sectors with many minimum wage roles

Businesses with a high proportion of minimum wage roles need to combine careful rota planning with margin analysis. The USC band changes help staff retain more of their increased pay, which can support recruitment and retention in competitive labour markets.Our budgeting and forecasting work in these sectors often includes sensitivity analysis for different sales volumes and wage cost scenarios. This helps management identify viable pricing, staffing and productivity strategies.

Higher‑wage sectors and USC leakage

For higher‑wage sectors, the minimum wage shift is less significant, but USC band thresholds still influence effective tax rates, especially around the €70,044 break into the 8% band. Salary rises that push staff above this level can lead to disproportionate USC increases if not planned.We help employers design salary reviews that consider both gross and net outcomes, supporting fair and sustainable reward structures in a changing USC environment.

The combination of a higher minimum wage, altered USC bands and extended credits means that both households and businesses benefit from structured planning. For individuals, this may involve revisiting savings goals, pensions and debt repayments in light of changed net income.

Planning Ahead: Tax, Budgeting and Advisory Around Budget 2026

For businesses, 2026 is an appropriate time to update financial projections and refine cash flow planning, especially where payroll is a large share of costs. We often combine Budget 2026 updates with broader advisory engagements on profitability and growth.

Using tax planning to maximise the benefit of the wage rise

Tax planning can help workers and business owners keep more of the gains from the new wage and USC settings. This may include optimised pension contributions, timing of bonuses and structured remuneration packages.We review each client’s situation, taking into account income sources, family circumstances and long‑term goals. In many cases, modest adjustments to how income is drawn can produce meaningful tax and USC savings.

Budgeting for wage and USC impacts in SMEs

SMEs often face tighter margins and less flexibility than larger organisations. We usually recommend a structured budgeting process that explicitly factors in:- Higher gross payroll costs from €14.15 per hour and knock‑on wage adjustments.

- Any expected changes in sales volumes or prices.

- Cash flow timing, especially for seasonal businesses.

Did You Know?

Budget 2026 delivers a total package of about €9.4 billion, with roughly €8.1 billion in spending and €1.3 billion in tax measures, including the €14.15 minimum wage and USC band changes.

Practical Checklist for 2026: Workers and Employers

For workers on or near minimum wage, the main priority is to understand expected net income under the €14.15 rate and updated USC bands, then plan budgets accordingly.

For employers, the priority is timely payroll updates and financial planning.

These steps provide a practical framework for navigating Budget 2026 rather than reacting in a hurry once the changes take effect.

Checklist for employees and self‑employed individuals

- Confirm your expected hourly rate or salary from January 2026 and how it compares to €14.15.

- Estimate your annual income and identify which USC bands will apply to you.

- Review eligibility for Rent Tax Credit, Mortgage Interest Relief or reduced USC as a medical‑card holder.

- Consider meeting a tax advisor to explore pension and tax planning options.

Checklist for employers and business owners

- Update all minimum wage roles to at least €14.15 per hour and adjust related rates.

- Implement new USC bands in payroll software and test January 2026 payroll runs.

- Refresh financial forecasts to reflect higher wage costs and any pricing changes.

- Communicate with staff about expected net pay and the role of USC bands.

Conclusion

The minimum wage rise to €14.15 and the associated USC band changes in Budget 2026 will reshape how income flows between workers, employers and the Exchequer.For minimum wage earners, the adjusted 2% USC band is crucial, since it preserves most of the gain from the higher hourly rate.

For employers and self‑employed individuals, the key is early planning.

By updating payroll systems, revising budgets and taking advantage of available tax credits and reliefs, it is possible to manage higher wage costs while supporting staff and maintaining financial stability.